Flood Insurance 101

Jul 12, 2018, 3:43 PM

Floods are the most common and most destructive natural disaster in the United States. According to the National Association of Insurance Commissioners, 90% of natural disasters involve some type of flooding. Even deserts see flood disasters and every Utahn should be aware that homeowners insurance and renters insurance do not cover damage from a flood. Before you’re cleaning water, mud or worse out of your home, take a minute to learn about flood insurance.

Do I need flood insurance?

If you live in a designated flood zone you are required to have flood insurance. If you live outside of those zones, flood insurance is optional but a good thing to consider. Take a look at your home and determine if it could be at risk of flooding from melting snow, overflowing creeks or ponds or water or mud coming down a steep hill or mountainside. If any of those scenarios seem possible, you should consider buying flood insurance. You can also check your address on FEMA’s Flood Map Service Center to see the flood hazard rating in your neighborhood.

If you live in a designated flood zone you are required to have flood insurance. If you live outside of those zones, flood insurance is optional but a good thing to consider. Take a look at your home and determine if it could be at risk of flooding from melting snow, overflowing creeks or ponds or water or mud coming down a steep hill or mountainside. If any of those scenarios seem possible, you should consider buying flood insurance. You can also check your address on FEMA’s Flood Map Service Center to see the flood hazard rating in your neighborhood.

Is it expensive?

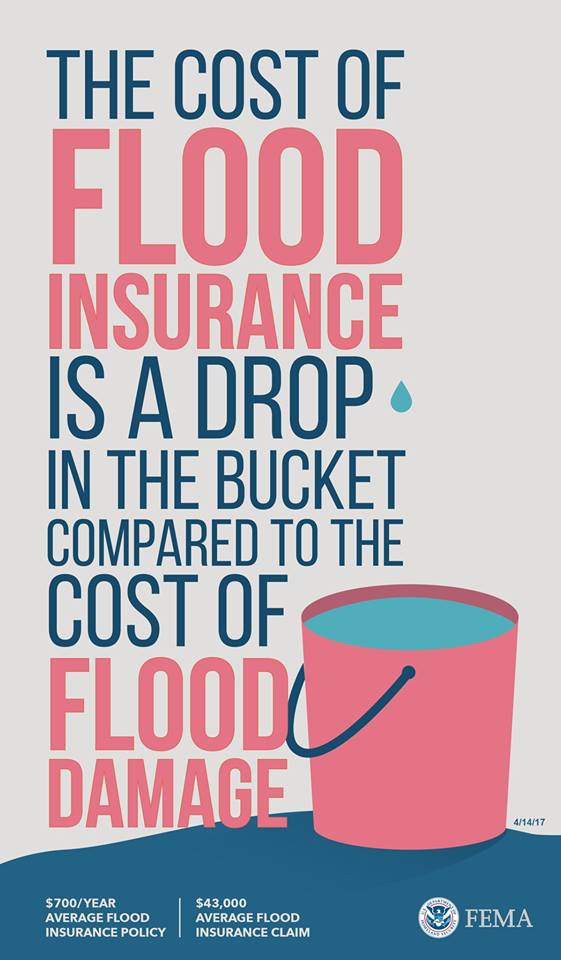

The Federal Emergency Management Agency (FEMA) estimates the average flood insurance policy in the United States is $700 per year bur prices can vary drastically depending on how close you live to water. Even just a few inches of water can cause tens of thousands of dollars in damage though. FEMA also estimates the average cost of a flood insurance claim is $43,000.

Where can I get flood insurance?

Most flood insurance is backed by the federal government as part of the National Flood Insurance Program. The insurance agent who helps you with your current home or rental insurance may be able to help you purchase that insurance so your first step is to check with them. If the agent can’t help you, you can contact the NFIP Help Center at 1-800-427-4661.

What is covered by flood insurance?

The cause of the flooding is important to know if the damage is covered. For example, damage caused by a sewer backup is only covered by flood insurance if that sewer backup is a result of flooding, not if its caused by another problem. Most policies cover damage and losses resulting from flood, flood-related erosion caused by heavy rain, snow melt, blocked storm drainage systems, and dam failure. To be considered a flood, water must cover at least two acres and affect two or more properties.

Flood insurance is sold in two types of policies, “building” and “contents”. Personal belongings are not covered if you only purchase a structure policy. There are options for combination policies.

Under “building” coverage you can typically expect eletrical and plumbing systems to be covered along with furnaces, water heaters, major kitchen appliances, carpet, drywall, bookcases and cabinets.

Some of the main items covered by “contents”include clothing, furniture, electronics, washers and dryers, and certain valuables.

How do I file a flood insurance claim?

Call your insurance agent as soon as possible and report your loss. You can also ask about an advance or partial payment to begin repairs or purchasing replacement items immediately.

Prepare for your insurance adjuster’s visit by documenting your loss. Take as many photos/videos of your damaged property as possible.

When your adjuster arrives they will inspect your property and create a detailed, room-by-room cost estimate and proof of loss form.

Finally, if you agree with the estimate, you will complete and sign a proof of loss report.

This Flood Claims Process Fact Sheet can also guide you through the process.