Feds Delay Payday Loan Rule: Here’s What You Should Know

Apr 4, 2019, 6:46 PM | Updated: Feb 7, 2023, 11:18 am

SALT LAKE CITY, Utah — In 2017, federal regulators issued a rule saying payday loan lenders have to verify a borrower’s ability to repay the loan. Recently, the Consumer Financial Protection Bureau put that rule on hold.

Here are three things you should know about payday loans.

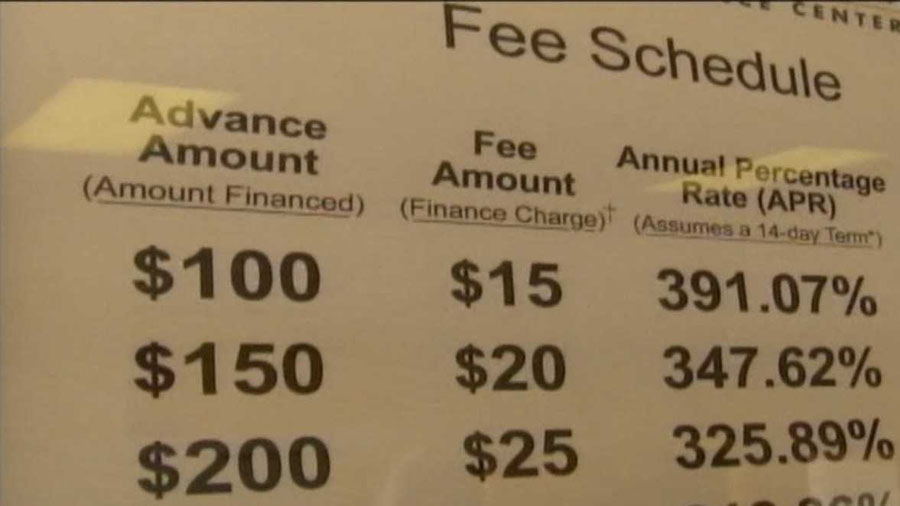

First, they have extremely high interest rates. Payday loan fees run from ten to $30 dollars for every hundred dollars borrowed. The annual interest rate on that works out to be from 261% to 782%.

Next, you need to pay off the entire loan plus fees in two weeks. Lenders typically do not offer payday loans with monthly installments like a car loan.

You can get an extension, but you will have to pay fees with every extension. On a $300 loan with a $60 fee ($20 for every hundred borrowed), extending the loan two months adds up to a total of $240 interest ($60 multiplied by 4 two-week pay periods.) And, you will still owe the original $300.

But, there are alternatives.

Financial experts say using a credit card is one possibility. It is not exactly ideal to rack up debt, but the interest will be significantly lower than a payday loan. However, if the card is maxed out or you don’t have one, consider applying for a personal loan from a bank or a credit union – if you have average to good credit.

If your credit is below that mark, a peer-to-peer lender typically has lower lending requirements but far lower interest rates than payday lenders will offer.

Another option is a payday alternative loan offered by members of the National Credit Union Association. Backed by the federal government, these loans offer borrowers with poor to average credit loans with APRs below 30% with terms of one to six months as opposed to two weeks typically offered by payday lenders.