Gephardt Busts Inflation: How balance transfer credit cards can help you climb out of debt

May 2, 2022, 9:37 PM | Updated: Jun 19, 2022, 9:54 pm

SALT LAKE CITY — Being in debt is stressful enough, let alone in times of rising inflation. But experts say one of the most powerful tools out there for controlling debt is not being used by people in debt over some common misconceptions.

A balance transfer lets you move debt from one account to another. To that end, many balance transfer credit cards allow someone to tack their existing debt onto a new credit card with 0% interest for 15, 18, and 21 months.

There is a great “Get Out of Debt” tool that is largely going unused because people are afraid of it, according to new data shared with @KSLInvestigates. I’ll break it down on @KSL5TV News at 6PM. pic.twitter.com/gO1UCJ5rpA

— Matt Gephardt KSL-TV (@KSLGephardt) May 2, 2022

“It’s one of the best weapons that you have in your arsenal for fighting credit card debt,” said Matt Schulz, LendingTree’s chief credit analyst.

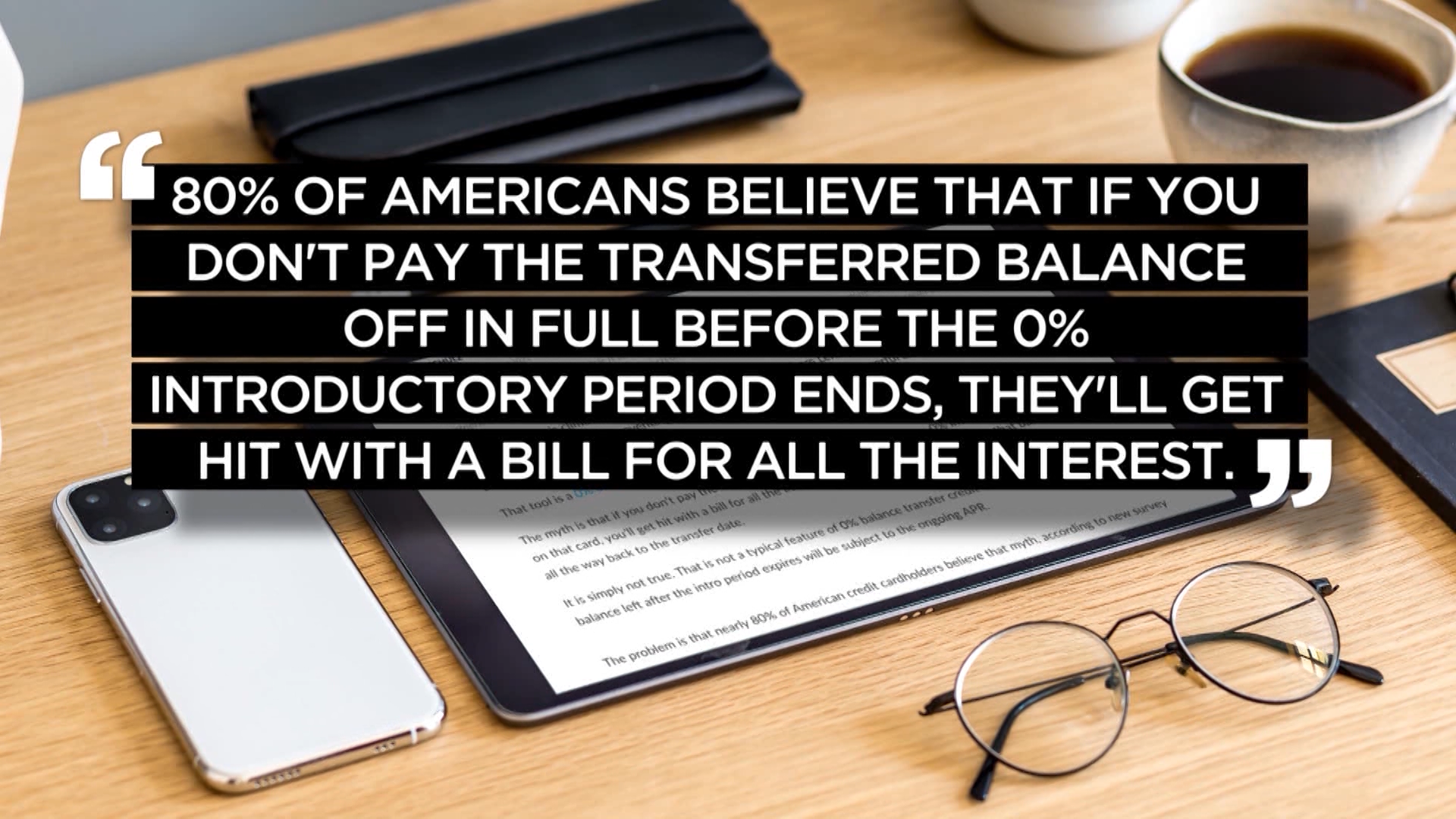

Schulz shared some surprising data with the KSL Investigators: Balance transfers are largely going un-weaponized. Eighty percent of Americans believe that if you don’t pay the transferred balance off in full before the 0% introductory period ends, they’ll get hit with a bill for all the interest. That is a myth, Schulz said.

“It’s pretty shocking how many people have this misconception,” he said.

Schulz explained that it is scaring a lot of people who would benefit from such cards away from using them.

“It is definitely not a get-out-of-jail-free card, you still have to pay that balance off,” he said. “But what a balance transfer credit card does is it can dramatically decrease the amount of interest you pay on that balance. So, it’s a really good thing.”

Another myth is that opening a new credit card will hurt your credit score, but Schulz said the truth is, it could actually lift up your credit score more than it hurts as you decrease your debt ratio.